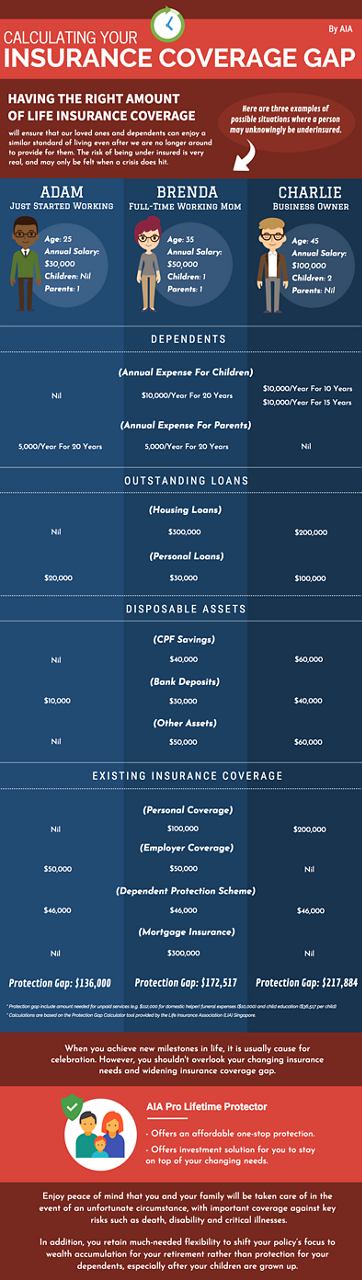

You want to ensure that your loved ones continue being able to live a similar standard of living even if you are no longer around. This is especially crucial if they were dependent on your income. To do this, you need to identify relevant costs areas, and plug any coverage gaps that you may have.

Here are some cost areas that you need to provide adequate coverage for.

# 1 Final costs

In the situation you pass on, your dependents will need to take care of your final costs. If you have diligently kept an emergency fund, that could go towards paying for this expense. According to the Life Insurance Association (LIA), average funeral costs is estimated to be close to $10,0001.

# 2 Unpaid Services

Unpaid services refer mainly to the household chores and caregiving duties, to children, other adults, or elderly parents, who you provide. In your absence, your family may have to hire a domestic or healthcare worker to do them.

The LIA estimates this cost to be close to $286,000 per working adult1.

# 3 Loans

Your loans include personal loans, car loans, housing loans, credit card debt and any other debts or loans that your dependents will need to pay off, either by taking over or using your assets.

The LIA has calculated the average outstanding loan for working adults to be an estimated $208,0001.

# 4 Children

If you have young children, they have ongoing needs, including university tuition fees, enrichment classes, food, clothing, and entertainment among others.

Typically, you should plan for your children to become financially independent only after they turn 20. The LIA estimates that each working adult will need to cater an estimated $79,000 for their children. This is based on average households in Singapore, which means that if you have more children, you should expect greater coverage needs1.

# 5 Elderly parents

If you have parents or parents-in-law that are dependent on your income on a daily basis, you need to ensure that your coverage is sufficient to provide for them. You need to take into consideration their life expectancy and standard of living as well.

LIA estimates that average working adults require $62,000 in coverage for elderly dependents1.

# 6 Surviving adults

The needs of the surviving adults is broken down into two cost components – rent and future household expenses.

Rents need to be considered for both elderly parents and spouses. LIA estimates the rent liabilities of each working adult to be $54,0001. Of course, this could be more or less depending on your unique situation.

The second cost component is the future household expenses, allowing for inflation. This excludes rent, children and elderly dependents, as they have been separately calculated in earlier cost components.

LIA estimates that working adults will have to provide for household expenses of $855,0001.