Multiple Primary Cancers Coverage under AIA HealthShield Gold Max Standard Plan

Updates & FAQs

No results found

Latest policy updates

Latest policy updates

23 FEBRUARY 2024

Protect your Policy Benefits with Claims Recovery

21 AUGUST 2023

Premium revision of VitalHealth A & VitalCare – 1 Sep 2023

15 AUGUST 2023

Updates on Shield's coverage for cancer drug treatment

12 DECEMBER 2022

Cancer drug treatment and services

The Cancer Drug Treatment (CDL) Benefit covers cancer drug treatments on the Cancer Drug List ("CDL"), up to the treatment-specific claim limits. If a cancer drug treatment is not listed or not administered exactly as described in the CDL, or if it is not found on CDL ("Non-CDL treatments"), it will not be claimable under this benefit.

If you are currently undergoing cancer drug treatment, you are encouraged to consult your doctor to understand whether your treatment is on the CDL.

Cancer Drug Services Benefit covers services that are part of a cancer drug treatment, such as consultations, scans, lab investigations, treatment preparation and administration, supportive care drugs and blood transfusions. For avoidance of doubt, patients may claim for Cancer Drug Services Benefit even if the service was rendered for a cancer treatment not on the CDL (i.e. Non-CDL treatments).

Insureds covered under riders with Cancer Care benefits are able to enjoy higher limits for both benefits and claim up to S$200,000 per policy year for selected Non-CDL treatments.

All claims are subject to a 10% co-insurance.

To keep cancer treatments and insurance premiums affordable in the longer term, CDL is introduced by the Ministry of Health of Singapore (MOH). The CDL comprises clinically proven and more cost-effective cancer drug treatments (i.e drugs paired with specified clinical indications, dosage form & strength, for which the drugs can be administered).

A treatment is approved for clinical use if it has met the regulatory authority's [in the case of Singapore, the Health Sciences Authority's (HSA's)] required standards of safety, quality and efficacy. A treatment is cost-effective if its clinical benefits commensurate with its costs. For more information, please refer to the FAQs on MOH's website at https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/what-medishield-life-benefits/cancer-drug-list.

The CDL is published on MOH's website at https://go.gov.sg/moh-cancerdruglist. MOH updates the CDL every few months to keep up with medical advancements and the latest clinical evidence.

Through the CDL, MOH can negotiate better prices and extend subsidies for more cancer drugs. More than 80% of subsidised cancer patients in Public Health Institutions (PHI) will now be able to access a wider range of subsidised cancer drug treatments than before. These changes aim to keep cancer drug treatments and insurance premiums affordable in the longer term.

MediShield Life (MSHL) and MediSave (MSV) cover treatments on the CDL from 1 September 2022.

For Integrated Shield Plan (IP), such as AIA HealthShield Gold Max, and its riders, the CDL came into effect from 1 April 2023, when an existing policy is renewed, or a new policy is purchased.

You may check with your doctor if the treatment is on the Cancer Drug List (CDL).

You can also visit the MOH's website at https://go.gov.sg/moh-cancerdruglist to view the latest version of the CDL. The list contains information on subsidies (if applicable), MediShield Life and MediSave claim limit for each treatment (i.e., drug indication pair).

No, they are not.

If the Insured undergoes a cancer drug treatment not listed on the CDL ("Non-CDL treatment"), the Non-CDL treatment will only be covered if he has a rider with Cancer Care Benefits. The Cancer Care Benefits covers for drug classes A, B, C, D1 to D3 and E1 to E3 (based on the LIA Non-CDL classification framework) up to S$200,000 per policy year, subject to a 10% co-insurance for every claim.

LIA Non-CDL classification framework: https://www.lia.org.sg/media/3553/non-cdl-classification-framework.pdf

Under AIA HSG Max, the claim limit will be a multiple of the MediShield Life (MSHL) claim limit for cancer drug treatment on the Cancer Drug List (CDL). For the MSHL Limit, please refer to the MOH's website at https://go.gov.sg/moh-cancerdruglist. 10% co-insurance applies for each claim.

| HSG Max A HSG Max B* HSG Max B Lite* |

HSG Max Standard*^ | |

|---|---|---|

| Outpatient Benefit: | ||

| Cancer Drug Treatment on the CDL (monthly limit) |

5 times of MSHL limit | 3 times of MSHL limit |

| Cancer Drug Services (yearly limit) |

5 times of MSHL limit | 2 times of MSHL limit |

* Pro-ration factor applies for treatment in Private hospital/any other private medical institution.

^ Patients receiving treatment for multiple primary cancers can receive higher coverage under the Cancer Drug Treatment on the CDL Benefit and Cancer Drug Services Benefit with effect from 1 April 2024, when an existing policy is renewed, or a new policy is purchased. Please click here for further information on multiple primary cancers coverage under HSG Max Standard plan.

The Insured will also be covered with additional coverage as follow if he is also covered under AIA HSG Max rider with Cancer Care benefits:

| AIA Max A Cancer Care Booster (attachable to AIA HSG Max A) | ||

|---|---|---|

| Without AIA Max VitalCare# / AIA Max VitalHealth (A / A Value) | With AIA Max VitalCare# / AIA Max VitalHealth (A / A Value) | |

|

16 times of MSHL limit (Less 10% co-insurance for every claim##) |

16 times of MSHL limit (Subject to the respective rider's co-payment and co-payment cap per policy per year@) |

|

10 times of MSHL limit (Less 10% co-insurance for every claim##) |

10 times of MSHL limit (Subject to the respective rider's co-payment and co-payment cap per policy per year@) |

|

S$200,000 (Less 10% co-insurance for every claim) |

S$200,000 (Less 10% co-insurance for every claim) |

The above cancer coverage will not be applicable to AIA HSG Max A policyholders if the AIA Max A Cancer Care Booster is not attached.

| AIA Max VitalHealth B AIA Max VitalHealth B Lite |

|

|---|---|

|

10 times of MSHL limit (Subject to the respective rider's co-payment and co-payment cap per Policy Year@) |

|

8 times of MSHL limit (Subject to the respective rider's co-payment and co-payment cap per Policy Year@) |

|

S$50,000 (Less 10% co-insurance for every claim) |

# Withdrawn plan (not available for new business or for switching in).

## The co-insurance will be capped at $50,000 per Policy Year if treatment is: by AIA Preferred Providers / pre-authorised / due to Emergency Confinement.

@ The co-payment is: 10% / 5% per claim and will be capped at S$6,000 / S$3,000 per policy year (for AIA Max VitalHealth A Value for treatment in private hospital / restructured hospital respectively); or 5% per claim and will be capped at S$3,000 per policy year (for the rest of the riders). The co-payment will be capped per Policy Year if treatment is by AIA Preferred Providers / pre-authorised / due to Emergency Confinement.

^ After pro-ration factor for treatment in Private hospital.

* Only Non-CDL treatments under selected drug classes A, B C, D1 to D3 and E1 to E3 of the LIA's Non-CDL Classification Framework are covered. For Non-CDL treatments, there is no coverage for the co-insurance incurred, nor is there stop-loss / co-payment cap for the co-insurance incurred; and the co-insurance incurred will not count towards the prevailing stop-loss / co-payment cap under the Deductible & Co-insurance Benefits.

LIA Non-CDL classification framework: https://www.lia.org.sg/media/3553/non-cdl-classification-framework.pdf

If multiple cancer drug treatments are administered for the same single primary cancer in a month, the maximum claim payable under the Cancer Drug Treatment on the CDL Benefit shall be up to the highest claim limit among the claimable CDL treatments received in that month.

In addition, drug omission or replacement with another CDL drug indicated "for cancer treatment" is allowed for multiple cancer drug treatments listed on the CDL only if it is due to intolerance or contraindications. In such cases, the claim limit of the original CDL treatment will apply.

If you are uncertain on whether your outpatient cancer treatment is considered a CDL treatment, please consult your doctor.

In this illustration, Acalabrutinib is claimable under drug treatment on CDL as it is prescribed for the cancer type and indication in accordance with CDL as follow:

- Cancer type: Leukaemia

- Indication: Monotherapy for previously untreated chronic lymphocytic leukaemia (CLL)/small lymphocytic lymphoma (SLL) in patients who are unsuitable for fludarabine-based therapy.

Claim Illustration for cancer drug treatment on CDL

CDL treatment: Acalabrutinib in a Private hospital / clinic

Plan: AIA HealthShield Gold Max A + optional AIA Max A Cancer Care Booster

| MediShield Life (MSHL) Claim Limit^ | AIA Claim Limit | |||

|---|---|---|---|---|

| AIA HealthShield Gold Max A^^ | Optional AIA Max A Cancer Care Booster ^^ | Total Claim Limit | ||

| Cancer Drug treatment on the CDL (monthly limit) | $2,000 | $10,000

(5 x MSHL)

|

$32,000 (16 x MSHL) |

$42,000 (21 x MSHL) |

| Cancer Drug Services (yearly limit) | $3,600 | $18,000 (5 x MSHL) |

$36,000 (10 x MSHL) |

$54,000 (15 x MSHL) |

^The MSHL's Cancer Drug Treatment on CDL claim limit listed above is correct as of 1 January 2024. The MSHL's Cancer Drug Services claim limit listed above is effective from 1 April 2023.

^^ (1) Payout under AIA HealthShield Gold Max A and AIA Max A Cancer Care Booster's Cancer Drug Treatment on CDL & Cancer Drug Services is subject to 10% co-insurance (up to 5% is covered under AIA Max VitalHealth / AIA Max VitalCare (if attached), subject to the prevailing co-payment per claim and co-payment cap per policy year). (2) If AIA Max VitalHealth / AIA Max VitalCare is not attached, the 10% co-insurance incurred per claim will be capped at $50,000 per policy year if treatment is: by AIA Preferred Providers / pre-authorised / due to Emergency Confinement.

The Cancer Drug Treatment (CDL) benefit will only cover cancer drugs administered as per the clinical indications specified in the CDL on the Ministry of Health of Singapore's website (https://go.gov.sg/moh-cancerdruglist). Any drug that is on the CDL but used for a different indication than what is specified on the CDL, will be considered as a Non-CDL treatment and it will not be claimable under the Cancer Drug Treatment (CDL) benefit under the AIA HealthShield Gold Max policy.

Example

The clinical indication for cancer drug A on the CDL is for a specific type of lung cancer for the treatment of locally advanced or metastatic EGFR mutation-positive non-small-cell lung cancer. Drug A shall not be considered as a CDL treatment if it is used for the treatment of other types of cancer and not claimable under AIA HealthShield Gold Max policy when the drug and indication pairing does not match the CDL.

Multiple cancer drug treatments administered in a month:

- Where multiple cancer drug treatments are administered in a month, and if any of the CDL treatments has an indication that states "monotherapy", only CDL treatments with the indication "for cancer treatment" will be claimable in that month.

Example:

CDL Treatment A ("monotherapy") + CDL Treatment B ("for cancer treatment") + CDL Treatment C ("for cancer treatment")

The claimable treatments shall be B and C with indication of "for cancer treatment", where we shall pay up to the highest limit among B and C in that month.

- When there are cancer drug(s) with indication other than "for cancer treatment", only CDL treatments with the indication "for cancer treatment" will be claimable in that month.

Example:

CDL Treatment A ("for cancer treatment") + CDL Treatment B ("for cancer treatment") + CDL Treatment C (indication other than "for cancer treatment") + CDL Treatment D (indication other than "for cancer treatment")

Only treatment A and B are claimable as they have the indication "for cancer treatment", where we shall pay up to the highest limit among A and B in that month.

The above examples are for illustration and it is non-exhaustive. If you are uncertain about whether your outpatient cancer treatment is considered a CDL treatment, please consult your doctor.

For cancer drug treatment not listed on the CDL ("Non-CDL"), the treatment will only be covered if the insured has a rider with Cancer Care Benefits. Only drug classes A, B, C, D1 to D3 and E1 to E3 (based on the LIA Non-CDL classification framework) are covered, up to S$200,000 per policy year, subject to a 10% co-insurance for every claim.

LIA Non-CDL classification framework: https://www.lia.org.sg/media/3553/non-cdl-classification-framework.pdf

Insureds who are undergoing Non-CDL treatments may wish to discuss with their doctors on whether there are suitable alternative treatments on the CDL. However, if switching to a CDL treatment is not feasible and there are financial concerns, you can consider the following options:

- For subsidised patients, you may approach a Medical Social Worker (MSW) in the public healthcare institution (PHI) for financial assistance such as MediFund.

- For non-subsidised patients in a PHI or patients in a private medical institution, you may approach your doctor for referral to a PHI, where financial assistance may be available. The PHI's medical team will review your treatment plan and provide financial counselling (e.g., eligibility for subsidies) to assist and advise on the transfer.

Per current practice and MOH's advice, all outpatient cancer treatment claims will continue to be e-Filed.

However, as e-Filing is not available for Foreigner Shield plans, policyholders may submit their bills through AIA's ClaimsEZ system. To facilitate claims processing, the bill should be submitted with a doctor's memo to indicate the MediClaim drug code for CDL/NCDL and indication code.

Coverage for multiple primary cancers

Higher coverage for Cancer Drug Treatment on Cancer Drug List (CDL) and Cancer Drug Services for multiple primary cancers has been implemented by MOH under MediShield Life (MSHL) and Medisave (MSV) from 1 December 2023:

- For Cancer Drug Treatment on Cancer Drug List (CDL), the MSHL and MSV limits is the sum of the highest cancer drug limit amongst the claimable treatments received for each primary cancer; and

- For Cancer Drug Services, the MSHL and MSV limits will be doubled.

AIA will apply the same approach under AIA HSG Max Standard plan and provide higher coverage for multiple primary cancers with effect from 1 April 2024 (when an existing policy is renewed or a new policy is purchased). For the higher coverage to apply, the Insured's treating doctor needs to send the application form to MOH and AIA for assessment of MediShield Life and Integrated Shield Plan claims respectively.

| Outpatient Benefit | Patients receiving treatment for one primary cancer | Patients receiving treatment for multiple primary cancers |

|---|---|---|

| Cancer Drug Treatment on Cancer Drug List (CDL) | 3 x (MSHL's limit1 for one primary cancer per month) | Sum of the highest cancer drug treatment limit1 amongst the claimable treatments received for each primary cancer per month |

| Cancer Drug Services | 2 x (MSHL's limit2 for one primary cancer per policy year) | 2 x (MSHL's limit2 for multiple primary cancers per policy year) |

1 The Cancer Drug Treatment on the CDL benefit limit is based on a multiple of the MSHL limit for the specific cancer drug treatment. For the latest MSHL limit, refer to the Cancer Drug List (CDL) on the Ministry of Health of Singapore's website under "MediShield Life Claim Limit per month" (https://go.gov.sg/moh-cancerdruglist). The Ministry of Health of Singapore may update this from time to time. The revised list will be applicable to the Cancer Drug Treatment which occurred on and from the effective date of the revised list.

2 The Cancer Drug Services benefit limit is based on a multiple of the MSHL limit for Cancer Drug Services. For the latest MSHL limit for Cancer Drug Services, refer to "Cancer Drug Services" under the MediShield Life Benefits on the Ministry of Health of Singapore's website (https://go.gov.sg/mshlbenefits). The Ministry of Health of Singapore may update this from time to time. The revised limit will be applicable to the Cancer Drug Services incurred within the policy year of the revised limit.

'Multiple Primary Cancers' refers to two or more cancers arising from different sites and/or are of different histology or morphology group. The claim limits for patients receiving treatment for multiple primary cancers are accorded on an application basis; doctors are to send the application form to the MOH and AIA for review of MediShield Life and Integrated Shield Plan claims respectively.

The occurrence of the Diagnosis of Multiple Primary Cancers must be proven to our satisfaction at your own expense, and any such proof shall include the following:

- evidence provided by the appropriate Physician or Specialist as the case may be;

- appropriate medical investigations and/or reports including, but not limited to, clinical, radiological, histological and laboratory evidence; and

- such other documents as we may require.

AIA HSG Max Standard plan provides higher coverage for multiple primary cancers, where under:

- the Cancer Drug Treatment on the Cancer Drug List (CDL) Benefit, we will pay up to the sum of the highest limit among the claimable CDL treatments received for each primary cancer in that month; and

- the Cancer Drug Services Benefit claim limit is doubled within the policy year.

Illustration:

Insured who is diagnosed with lung cancer and brain cancer and prescribed the following treatment regimen. The total benefit payable under the Cancer Drug Treatment on the CDL Benefit and Cancer Drug Services Benefit are as follow:

| Cancer Drug Treatment on the CDL Benefit (monthly limit) |

Cancer Drug Services Benefit (yearly limit) |

||||

|---|---|---|---|---|---|

| MediShield Life (MSHL) Limit* |

AIA HSG Max Standard^ | MediShield Life (MSHL) Limit |

AIA HSG Max Standard^ | ||

| Lung Cancer | $1,000 | $3,000 (3X MSHL) |

$3,000 + $3,600 = $6,600 | $7,200^^ | $14,400# (2X MSHL) |

| Breast Cancer | $1,200 | $3,600 (3X MSHL) |

|||

*If multiple cancer drug treatments are administered for the same single primary cancer in a month, the maximum claim payable under the Cancer Drug Treatment on the CDL Benefit shall be up to the highest claim limit among the claimable CDL treatments received in that month.

^Payout under AIA HSG Max Standard's Cancer Drug Treatment on the CDL & Cancer Drug Services is subject to 10% co-insurance.

^^The MSHL's Cancer Drug Services Claim Limit listed above is correct as of 23 Feb 2024. For the latest MSHL limit for Cancer Drug Services, refer to "Cancer Drug Services" under the MediShield Life Benefits on the Ministry of Health of Singapore's website (https://go.gov.sg/mshlbenefits). The Ministry of Health of Singapore may update this from time to time.

# Higher Cancer Drug Services Benefit limit will apply to the services incurred in the Policy Year after assessment and approval from MOH and AIA on multiple primary cancers coverage. The higher limit will no longer apply in the next policy year unless there is an application for higher coverage on multiple primary cancers and it is approved by MOH and AIA.

Higher claim limits for patients receiving treatment for multiple primary cancers are accorded on an application basis. Patients can follow the steps below for AIA assessment.

- The treating doctor needs to send in the application form (Application for Higher MediShield Life and MediSave Limit for Patient with Multiple Primary Cancers), indicating the Insured's multiple primary cancers diagnosis and details of treatment for each primary cancer, to MOH and AIA for assessment of MediShield Life and HSG Max Standard plan coverage respectively, prior to the commencement of the treatment for multiple primary cancers.

- Once AIA receives the completed application form (Application for Higher MediShield Life and MediSave Limit for Patient with Multiple Primary Cancers) from the treating doctor, a Pre-authorisation request will be sent to the policyholder for authentication. Once you have authenticated the request, a pre-authorisation form will be automatically sent to the doctor for their completion.

- AIA will review and assess the completed pre-authorisation form and inform the policyholder on the coverage outcome for the planned treatment. Additional reports and documents may be required for the assessment.

You are strongly advised to submit your application for multiple primary cancers at least 1 month before your treatment commences.

Failure to complete the above may lengthen the process for assessment and reimbursement. We will only provide higher coverage for multiple primary cancers after the treatment regimen has been assessed and approved by us. Otherwise, the coverage will be based on the limits for "one primary cancer".

Deductibles and Co-insurance

A deductible is the amount you pay for covered health care services before your insurance plan starts to pay. With a $2,000 deductible, for example, you pay the first $2,000 of covered services yourself.

After you pay the deductible, you usually will need to pay the co-insurance / co-payment for covered services before your insurance starts to pay. The amount covered by the insurance plan, is subject to the deductible & co-insurance / co-payment.

Both deductibles and co-insurance / co-payment features help keep premiums affordable.

On co-payment

After paying the applicable deductible, policyholders will need to pay out-of-pocket of a minimum of 5% on their covered bills before the insurance pay-out can cover the expenses. This means that Integrated Shield Plan (IP) and rider will no longer cover 100% of medical bills.

Expenses that are not covered by AIA are not subject to the 5% co-payment as the full amount is already paid out-of-pocket by the policyholder.

On co-payment cap

The co-payment is capped at $3,000 (or $6,000 for VitalHealth Max A Value) per policy year, if the insured receives treatment from an AIA Quality Healthcare Partners (AQHP) specialist or a public hospital, or if the treatment is pre-authorised.

Note that for AIA Max VitalHealth & AIA Max VitalCare riders, the co-payment cap of S$3,000 is extended to include emergency confinement via A&E, even if the treating doctor is non-panel and/or without pre-authorisation.

The aim of the co-payment cap feature is to protect you against large bills by limiting the out-of-pocket amount you have to pay per policy year. The minimum co-payment cap insurers can apply is $3,000.

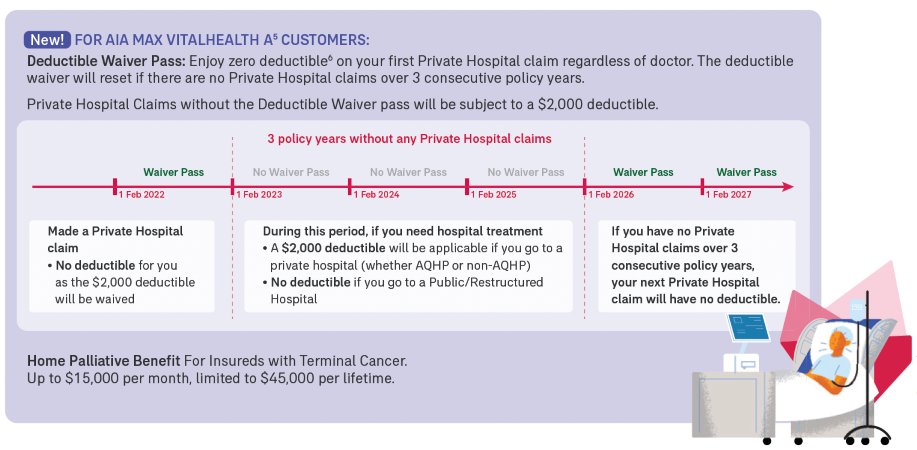

Deductible Wavier Pass is a feature under AIA Max VitalHealth A rider.

5Existing 'AIA Max Essential A Saver' plans will be known as 'AIA Max VitalHealth A'.

6Subject to 5% co-payment.

Customers and insurance representatives may refer to our customer portal or AgIA respectively to find out the Deductible Waiver Pass status at any time.

Claim-based pricing for AIA Max VitalCare

Claim-based pricing is a fairer pricing approach to empower our policyholders with more control over their future renewal premiums by managing their claim experience. Customers who make less claims will be rewarded with lower premiums.

It is applicable for AIA Max VitalCare only, which is not available for new business or for switching in from 1 April 2024. For more information on your AIA Max VitalCare Policy, please refer to your contract or approach your AIA Financial Service Consultant / Insurance Representative.

There are five premium levels in the claim-based pricing for AIA Max VitalCare.

With claim-based pricing, all policyholders will start off at the Standard Level premium, the lowest premium level of your age band. During each policy renewal, the renewal premium level will be determined by the previous claim made during the premium evaluation period. As long as you stay healthy, with no claims made during the premium evaluation period while your AIA Max VitalCare is at Standard Level, you will continue to enjoy the No Claim Discount on your Standard Level premium at your next policy renewal.

Claim-based pricing rewards customers who actively manage their health and are judicious in their use of medical services.

When no claims are made during the premium evaluation period, and if the AIA Max VitalCare is at Standard Level Premium, policyholders will get to enjoy a specified discount rate. The No Claim Discount applies only to the AIA Max VitalCare premium, and will increase based on the number of years without claim.

The No Claim Discount will increase if no claims are made for subsequent Premium Evaluation Periods, up to 25%.

AIA Max VitalCare is the only AIA IP rider which is subject to claim-based pricing.

Customers who do not want to be subject to claim-based pricing may consider switching to AIA Max VitalHealth A or AIA Max VitalHealth A Value riders.

When contemplating switching, customers should consider factors like age, pre-existing conditions, appropriate healthcare for your needs and affordability of future premiums. It is important to understand the risk of switching plans, as this could lead to an exclusion of pre-existing conditions or an increase in premiums (loading).

Customers are encouraged to speak with your AIA Financial Services Consultant / Insurance Representative and he/she will be able to advise further based on your existing portfolio and health insurance needs.

Currently, only AIA Max VitalCare is subject to claim-based pricing. AIA Max VitalCare is a rider that is only attachable to the AIA HealthShield Gold Max A plan.

In implementing claim cost containment initiatives, we have always prioritised initiatives that will truly be effective without affecting the adequacy of the protection we provide. We will monitor and review the new claim-based pricing approach closely to ensure that we continue to strengthen our comprehensive healthcare proposition in a meaningful way.

As a leading insurer in the healthcare space, AIA Singapore is committed to journeying with our customers through their lives as well as continuously providing them with innovative solutions that truly meet their needs.

Your premium level may move up or down depending on the source of claim and the claim amount paid from your AIA Max VitalCare during each policy year. This is assessed and determined during the Premium Evaluation Period.

For the very first renewal of AIA Max VitalCare, the Premium Evaluation Period will cover the first 10 months from the issue date or renewal date of AIA Max VitalCare.

For subsequent renewals of AIA Max VitalCare, the Premium Evaluation Period will be a period of 12 months commencing from the date immediately following the previous Premium Evaluation Period.

For example, if the previous Premium Evaluation Period ended on 8 November 2020, the subsequent Premium Evaluation Period shall be from 9 November 2020 to 8 November 2021.

Your premium level may move up or down depending on the source of claim and the claim amount paid from your AIA Max VitalCare during each policy year. This is assessed and determined during the Premium Evaluation Period.

Please be assured that you will be notified of the premium level in your next renewal through the yearly Premium Notification Letter, and you can also access the information through our customer portal.

Yes. The Standard Level Premium rates are not guaranteed and are expected to be adjusted from time to time to allow for ongoing reviews of claims experience, medical inflation, and general cost of treatments, supplies or medical services in Singapore.

When there were claims made for both private hospital and restructured hospital treatment during the premium evaluation period, only private hospital claims made will be used to ascertain the next renewal premium level for AIA Max VitalCare.

With claim-based pricing, you will start off at the Standard Level premium, the lowest premium level of the relevant age band. During each policy renewal, the renewal premium level will be determined by the previous claims made during the premium evaluation period. Any changes to your premium level will be implemented on your next policy renewal.

The lock in date for AIA Max VitalCare's renewal premium level is T - 2 calendar months, where T is the next policy anniversary date.

Switching of riders

How does switching across riders work?

You may request to switch to other riders by making a request for change. Please note that your request may be subject to underwriting.

With effect from 1 April 2024, the following will apply:

Existing AIA Max VitalCare policyholders may switch to:

- AIA Max VitalHealth A, AIA Max VitalHealth A Value, AIA Max VitalHealth B or AIA Max VitalHealth B Lite – No underwriting is required.

Existing AIA Max VitalHealth A policyholders may switch to:

- AIA Max VitalHealth A Value, AIA Max VitalHealth B or AIA Max VitalHealth B Lite – No underwriting is required.

Existing AIA Max VitalHealth A Value policyholders may switch to:

- AIA Max VitalHealth A - Underwriting is required.

- AIA Max VitalHealth B or AIA Max VitalHealth B Lite – No underwriting is required.

Existing AIA Max VitalHealth B policyholders may switch to:

- AIA Max VitalHealth A or AIA Max VitalHealth A Value - Underwriting is required.

- AIA Max VitalHealth B Lite – No underwriting is required.

Existing AIA Max VitalHealth B Lite policyholders may switch to:

- AIA Max VitalHealth A, AIA Max VitalHealth A Value or AIA Max VitalHealth B - Underwriting is required.

Existing AIA Max Essential C policyholders may switch to:

- AIA Max VitalHealth A, AIA Max VitalHealth A Value, AIA Max VitalHealth B or AIA Max VitalHealth B Lite - Underwriting is required.

Note: upon switching of riders, the basic plan will be switched accordingly.

When contemplating switching, please do consider factors like age, pre-existing conditions, appropriate healthcare for your needs and affordability of future premiums. It is important to understand the risk of switching plans, as this could lead to an exclusion of pre-existing conditions or an increase in premiums (loading). Speak with your AIA Financial Services Consultant / Insurance Representative and he / she will be able to advise further based on your existing portfolio and health insurance needs.

Early Detection Screening Benefit

We introduced the Early Detection Screening Benefit for AIA HealthShield Gold Max with rider* in 2019 as part of our efforts to help our customers stay healthy and manage their health for the long term. Appropriate screening can help to detect potentially serious medical condition(s) in advance to facilitate early diagnosis and treatment, helping you to lead a healthier, longer and better life.

You may also refer to our website for more information.

*Applicable only for AIA Max VitalHealth A and AIA Max VitalCare riders.

All insured customers under the following plans who have reached the eligibility age* on the policy anniversary are entitled to the Early Detection Screening Benefit:

- AIA Max VitalHealth A

- AIA Max VitalCare

In addition, the rider must have been in-force for at least 2 consecutive years and the premiums for the next policy year must have been duly paid and received by AIA.

*Please refer to Question 3 for the age criteria.

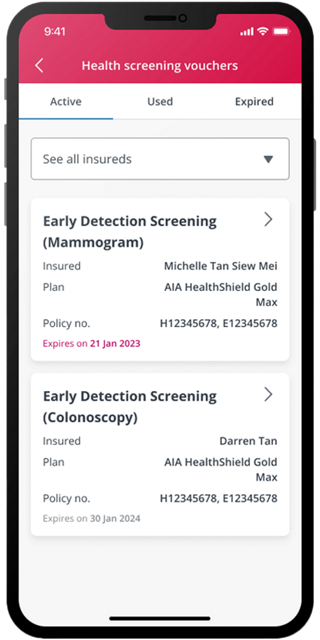

The screenings available under the Early Detection Screening Benefit are:

No.

|

Screening

|

Insured Eligibility

|

Frequency

|

1.

|

Colonoscopy

|

Males and Females, age 50 and above

|

Every 10 years from the policy year of the last screening voucher's issuance date

|

2.

|

Mammogram

|

Females, age 40 to 69

|

Every 2 years from the policy year of the last screening voucher's issuance date

|

The first screening voucher will be issued on the policy anniversary when the insured meets the eligibility criteria, or when the premium for the next policy year is paid and received by AIA, whichever is later.

Note: This Early Detection Screening Benefit is for healthy individuals, and is not intended for use by customers who have existing symptoms of breast or colorectal conditions, or who have a prior history of breast or colorectal conditions. Customers who are not eligible for the benefit are encouraged to continue their follow-up with their respective doctors. You may refer to the Terms and Conditions stated on the Early Detection Screening vouchers for more details.

No, this complimentary screening is optional. If you would like to go for the screening, please make an appointment with your preferred screening partner in advance.

You may utilise your benefit in 4 simple steps:

Step 1: Retrieve your voucher

Upon receiving SMS / email notification from AIA, you may login to customer portal to retrieve your screening vouchers.

Step 2: Make an appointment

Schedule an appointment with your preferred clinic/imaging centre from our list of participating screening partners.

Step 3: Go for your screening

Present the following upon registration at the clinic / imaging centre on the day of your screening

- AIA Early Detection Screening Voucher; and

- Your NRIC / FIN / Passport

Step 4: Collect your health report

Collect your health check report directly from the service provider.

The voucher has a validity period of 1 year (from policy anniversary date) and no extension is allowed.

To ensure that you secure your preferred appointment date and time, we strongly encourage you to make an appointment with your preferred screening partners listed in advance. You may reach them via voice call, SMS, WhatsApp, and/or Email as indicated on the list.

Coverage of further investigations and treatments will depend on whether these fall within the benefits of your AIA HealthShield Gold Max A policy, as well as any other applicable terms and conditions in your policy. The admissibility of claims for any such expenses will be assessed under and in accordance with the terms of the policy.

Home Palliative Benefit

Home Palliative care refers to the provision of palliative services in the patient's home. Common palliative services include changing of wound dressings, feeding tubes, stoma care, urinary tube changes, provision of supportive medicines and nutritional feeds.

Home Palliative care provides patients with greater sense of independent living and comfort in familiarity for terminally ill cancer patients. The Home Palliative care benefit provides coverage for eligible items up to $15,000 per month with maximum lifetime limit of $45,000.

Home Palliative Benefit is available to Insureds who are diagnosed with terminal cancer with expected survival period of 12 months or less under the following rider:

- AIA Max VitalHealth A

- AIA Max VitalHealth A Value

- AIA Max VitalCare

To apply for the service, you need a referral letter* from your oncologist to the AIA Appointed Home Palliative Care Provider(s).

Step 1: Insured requires home palliative care service

Step 2: Insured / referring oncologist contacts AIA Appointed Home Palliative Care Provider to submit referral letter*

Step 3: AIA Appointed Home Palliative Care Provider contacts the insured.

Step 2: Insured / referring oncologist contacts AIA Appointed Home Palliative Care Provider to submit referral letter*

Step 3: AIA Appointed Home Palliative Care Provider contacts the insured.

*Note: The referral letter must include a declaration that the insured is diagnosed with Terminal Cancer with an expected survival period not exceeding 12 months.

Please see the table below for the Appointed Providers for this service.

Note: This list of Appointed Providers is correct as of 01 September 2023 and may be subject to change.

The Home Palliative benefit covers eligible items - doctor's attendance fee, nurse's attendance fee, prescription drugs and/or supportive medicine (e.g. pain relief medications, total parenteral nutrition), medical consumables (e.g. wound dressings) and procedures (e.g. feeding tube changes, stoma wound care). If other items are required, AIA reserves the right to determine whether they are considered as Reasonable and Customary.

To submit a claim, the following criteria must be fulfilled:

- Service is provided by AIA Appointed Home Palliative Care Provider;

- Claim is accompanied by an oncologist's referral letter with declaration that the patient has Terminal Cancer with an expected survival period not exceeding 12 months;

- Claim is linked to a main claim episode for which the claim has been approved. This main claim episode may be an inpatient admission or an outpatient chemotherapy episode within the last six (6) months (Note: This is determined based on the date of the first Home Palliative claim);

- Claim is admissible only for eligible items required for the delivery of Home Palliative. Refer to question 5 for eligible items; and

- All claims submitted for Home Palliative benefit should be within 12 consecutive months from date of the first Home Palliative benefit claim, subject to the Limit of Compensation stated in the Schedule of Benefits.

AIA Preferred Providers

AIA Preferred Providers is any public hospitals which is approved by the Ministry of Health and any private medical service provider listed under AIA Quality Healthcare Partners (AQHP) in our website.

AQHP is our panel of private specialist doctors exclusively curated for AIA HealthShield Gold Max customers. Each of them has at least 5 years of specialist experience and a clean professional track record.

AIA HealthShield Gold customers who use medical services provided by AIA Preferred Panel will also get to enjoy higher benefits.

Introducing AIA Preferred Providers is one of the measures that the Company has put in place to manage rising healthcare costs. Such was one of the recommendations of the Health Insurance Task Force to ensure that health insurance premiums remain sustainable in the long run.

By using medical services provided by AIA Preferred Providers, AIA HealthShield Gold Max customers will enjoy the following enhanced benefits with their policy:

| Benefits | ||

|---|---|---|

| Treatment by AIA Preferred Providers# |

Treatment by Non-AIA Preferred Providers |

|

| Basic: AIA HealthShield Gold Max A | ||

|

Within 13 months before hospitalisation

|

Within 100 days before hospitalisation

|

|

Within 13 months after hospitalisation | Within 100 days after hospitalisation |

|

$2,000,000 | $1,000,000 |

| Rider: AIA VitalHealth A / B / B-Lite | ||

|

$3,000 per policy year*

|

N.A.^

|

| Rider: AIA VitalHealth A Value | ||

|

Private panel: $6,000 per policy year*

Restructured: 3,000 per policy year*

|

N.A.^

|

* Regardless of whether or not Certificate of Pre-authorisation is obtained.

^ Except if a Certificate of Pre-authorisation prior to treatment is obtained; or it is for Emergency Confinement that is referred by an Accident and Emergency Unit in Singapore. In any of such case, the same Co-payment Cap applies.

#When there are more than one physician treating the insured for the same hospitalisation, the main treating physician must be an AIA Preferred Provider.

Please refer to the respective contracts for the full terms and conditions.

Value-added services for AIA HealthShield Gold Max customers

What other value-added services do AIA HealthShield Gold Max customers enjoy?

AIA HealthShield Gold Max customers will enjoy the following value-added services*:

| Appointment requests with an AQHP specialist | Telemedicine | Personal Case Management | Option to integrate with AIA Vitality | |

|---|---|---|---|---|

| AIA HealthShield Gold Max A / B / B-Lite / C# | ✓ | ✓ | - | - |

| AIA VitalCare# | ✓ | ✓ | ||

| AIA VitalHealth A / A-value / B | ✓ | ✓ | ||

| AIA VitalHealth B-Lite / AIA Max Essential C# | - | - |

*Subject to terms and conditions.

#Withdrawn plan (not available for new business or for switching in).

Please refer to the respective links for more information.

AIA HealthShield claims

For Singaporeans (SGP) and Permanent Residents (PRs)

Claims are to be submitted to us through the system set up by the MOH in accordance with the terms and conditions under the CPF Act and the MediShield Life Scheme Act 2015 (where applicable), as amended from time to time. Once you have given the medical institution the authorisation to submit your claim for you, the medical institution will submit a claim to the insurer on your behalf.

This will not be applicable to claims under the following benefits:

- Pre-Hospitalisation Benefit

- Post-Hospitalisation Benefits

- Congenital Abnormalities of Insured's Biological Child from Birth (for female Insured)

- Non-insured Donating an Organ to Insured

- Medical Treatment outside Singapore Benefits

- Post-Hospitalisation Psychiatric Treatment

These claims must be made through our online claim submission portal 'ClaimsEz' and must be submitted to us within 60 days from the date the insured is discharged from the hospital or the date of receiving the outpatient treatment.

For Foreigners

Claims must be made through our online claim submission portal 'ClaimsEz' and must be submitted to us within 60 days from the date the insured is discharged from the hospital or the date of receiving the outpatient treatment.

For Total and Permanent Disability (TPD) claims:

Claims must be notified through the submission of a completed Disability Claim form and other proof of loss documents within 60 days from the date the insured satisfies the TPD definition as stated in our contract.

Please refer to the respective policy contract for the full terms and conditions.

It is defined as "any physical condition, impairment or the existence of any illness or disease that was diagnosed, treated, or for which a Physician or Specialist was consulted at any time prior to the Policy Date, or last reinstatement date (if any), whichever is later, unless declared in the Application form and specifically accepted by the Company".

For this purpose, an illness or disease has occurred when it has been investigated, diagnosed or treated or when signs or symptoms have manifested which would cause an ordinarily prudent person to seek Diagnosis, care or treatment.

Except in the case of an "Emergency" or planned medical treatment outside Singapore (as covered under the policy and subject to terms & conditions), overseas medical treatments are not covered

"Emergency" means a serious illness or injury or the onset of a serious condition, which in our opinion requires urgent remedial treatment to avoid death or serious impairment to the Insured's immediate or long-term health.

The MediSave accredited institution(s) / referral centre(s) and the contact details can be found on CPFB | Can I use my MediSave for overseas treatment/hospitalisation

The list is subject to any change made on the covered healthcare providers for approved hospitalisation by MediSave. Planned Medical Treatment outside Singapore will not be covered under AIA HealthShield Gold Max policy if a referral has not been obtained from a MediSave-accredited institution / referral centre in Singapore for approved overseas hospitalisation as covered by MediSave.

He needs to submit the original final hospital bill and a copy of our settlement letter to his company insurer to claim the balance of the hospital bill not covered under the integrated plan.

All medically necessary medications prescribed by the attending physician related to the hospitalisation is claimable, subject to the terms and conditions of the Policy. This does not include supplement, experimental drugs etc.

AIA HealthShield Gold Max covers the majority of your medical bill. Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total bill was $100K.

With AIA HealthShield Gold Max A

John pays deductible:

$3,500 |

|---|

John pays

co-insurance: $9,650 [10% x ($100,000 - $3,500)]

|

HSG Max A (including

MediShield Life) pays: $86,850 |

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalHealth A covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. As the policy has a Deductible Waiver Pass, John does not need to pay any deductible. With a certificate of pre-authorisation for his treatment, the co-payment payable by John will be capped at $3,000. Hence, John will pay $3,000 from his own pocket and the remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalHealth A (with Deductible Waiver Pass + Certificate of Pre-Authorisation)

AIA Max VitalHealth A

(which covers deductible and co- insurance) pays: $10,150 |

John pays

co-payment: $3,000 |

|---|---|

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalHealth A covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. As the policy does not have a Deductible Waiver Pass, John needs to pay $2,000 deductible from his own pocket. With a certificate of pre-authorisation for his treatment, the co-payment payable by John will be capped at $3,000 per policy year. Hence, John will pay a total of $5,000 from his own pocket and the remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalHealth A (No Deductible Waiver Pass but with Certificate of Pre-Authorisation)

| John pays deductible: $2,000 |

|

|---|---|

AIA Max VitalHealth A

(which covers the remaining deductible and co-insurance) pays: $8,150 |

John pays

co-payment: $3,000 |

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalHealth A covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. As the policy has a Deductible Waiver Pass, John does not need to pay any deductible. As treatment was not pre-authorised, the co-payment cap does not apply. Hence, John will pay a co-payment of $5,000 from his own pocket and the remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalHealth A (with Deductible Waiver Pass, No Certificate of Pre-Authorisation)

AIA Max

VitalHealth A (which covers deductible and co- insurance) pays: $8,150 |

John pays co-

payment: $5,000 |

|---|---|

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalHealth A covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. As the policy does not have a Deductible Waiver Pass, John would need to pay $2,000 deductible from his own pocket. As the treatment was not pre-authorised, the co-payment cap does not apply. Hence, John would need to pay a total of $6,900 from his own pocket. The remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalHealth A (with No Deductible Waiver Pass, No Certificate of Pre-Authorisation)

| John pays deductible: $2,000 |

|

|---|---|

AIA Max VitalHealth

A (which covers the remaining deductible and co- insurance) pays: $6,250 |

John pays

co-payment: $4,900 |

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalCare covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. With a certificate of pre-authorisation, the co-payment payable by John will be capped at $3,000. Hence, John only needs to pay $3,000 from his own pocket and the remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalCare (With Certificate of Pre-Authorisation)

AIA Max VitalCare

(which covers deductible and co- insurance) pays: $10,150 |

John pays

co-payment: $3,000 |

|---|---|

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalCare covers deductibles and co-insurance, subject to 5% co-payment.

Here is an example to illustrate*:

John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K. As the treatment was not pre-authorised, the co-payment cap does not apply. Hence, John would need to pay $5,000 from his own pocket. The remaining bill is covered under his policies.

With AIA HealthShield Gold Max A and AIA Max VitalCare (No Certificate of Pre-Authorisation)

AIA Max VitalCare

(which covers deductible and co- insurance) pays: $8,150 |

John pays co-

payment: $5,000 |

|---|---|

HSG Max A (including MediShield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max covers the majority of your medical bill while AIA Max VitalHealth A Value covers deductibles and co-insurance, subject to co-payment of up to 10%

Here is an example to illustrate*:

Example: John, who is covered under AIA HealthShield Gold Max A, was hospitalised in a private hospital. His total eligible bill was $100K.

With AIA HealthShield Gold Max A and AIA Max VitalHealth A Value (with Certificate of Pre-Authorisation).

As the treatment is from a private hospital, John needs to pay $3,500 deductible from his own pocket. With a certificate of pre-authorisation for his treatment, the co-payment payable by John will be capped at $6,000. Hence, John will pay a total of $9,500 from his own pocket and the remaining bill is covered under his policies.

John pays deductible:

$3,500 |

|

|---|---|

AIA Max VitalHealth

A Value (which covers the remaining deductibles and co- insurance) pays: $3,650 |

John pays co-

payment: $6,000 |

HSG Max A (including MediShield Life)

pays: $86,850 |

|

With AIA HealthShield Gold Max A and AIA Max VitalHealth A Value (No Certificate of Pre-Authorisation)

As the treatment is from a private hospital, John needs to pay $3,500 deductible from his own pocket. As the treatment was not pre-authorised, the co-payment cap will not apply. Hence, John will pay a total of $13,150 from his own pocket and the remaining bill is covered under his policies.

John pays deductible:

$3,500 |

|

|---|---|

AIA Max VitalHealth

A Value (which covers the remaining deductibles and co- insurance) pays: $0 |

John pays co-

payment: $9,650 |

HSG Max A (including MediShield Life)

pays: $86,850 |

|

However, should John be admitted to A Ward Class of a Restructured hospital, John does not need to pay any deductibles and there is a co-payment cap at $3,000 as shown below:

With AIA HealthShield Gold Max A and AIA Max VitalHealth A Value (A Ward Class of a Restructured hospital)

John pays deductible:

$0 |

|

|---|---|

AIA Max VitalHealth

A Value (which covers the remaining deductibles and co- insurance) pays: $10,150 |

John pays co-

payment: $3,000 |

HSG Max A (including Medishield Life)

pays: $86,850 |

|

* Please note that any claims on your policy would be subject to the terms and conditions of your policy contract.

AIA HealthShield Gold Max will cover Ptosis (subject to terms and conditions of your policy contract) only when the condition affects your field of vision or gives rise to a functional problem.

If the severity of ptosis fails to fulfil the intervention criteria set out by MOH or if the said intervention is meant for aesthetic purpose, it will not be covered under your AIA HealthShield Gold Max policy.

Others

Please contact your AIA Financial Services Consultant/Insurance Representative or call our AIA Customer Care Hotline at 1800 248 8000 to update your personal particulars.

You may consult your AIA Financial Services Consultant/Insurance Representative or call our AIA Customer Care Hotline at 1800 248 8000.

Alternatively, you can also access your policy details on the go via our customer portal.